Invoice financing is a powerful financial tool that can help businesses unlock the value of their outstanding invoices. By leveraging unpaid customer invoices, companies can access much-needed cash flow to cover expenses, invest in growth, or navigate financial challenges.

For many businesses, slow-paying customers and extended payment terms can create significant cash flow gaps. Invoice financing offers a solution by allowing companies to borrow against the value of their accounts receivable, providing a fast and flexible source of working capital.

In this article, we’ll dive into the fundamentals of invoice financing, exploring how it works, the different types available, and the benefits it can offer to businesses looking to optimize their cash flow management. Whether you’re a small business owner, a financial professional, or simply curious about alternative financing options, understanding invoice financing can open up new possibilities for growth and stability.

Automate document processing with TurboDoc

Recognize invoices, contracts, and forms in seconds. No manual work or errors.

Try for free!

What is invoice financing?

Invoice financing is a financial solution that enables businesses to borrow money against the value of their outstanding customer invoices. By leveraging the accounts receivable as collateral, companies can access a significant portion of the invoice amount—typically 70% to 95%—in as little as one to two days.

This type of financing is particularly beneficial for businesses that often face long payment cycles or have a substantial amount of working capital tied up in unpaid invoices. With invoice financing, companies can improve their cash flow position without taking on additional debt or giving up equity in the business.

The process is relatively straightforward: businesses sell their outstanding invoices to a financing company at a discount, receiving an immediate cash advance. The financing company then holds the remaining invoice value in reserve until the customer pays the invoice in full. Once the invoice is paid, the financing company collects its fees and releases the reserved funds to the business. Tools like TurboDoc can help streamline the invoice management process, making it easier for businesses to track and finance their receivables.

How does invoice financing work?

Invoice financing starts when a business submits its unpaid invoices to a financial provider, seeking liquidity before customer payments are made. The financing company evaluates the invoices and customer creditworthiness, then advances a portion of the invoice value, typically a significant majority. This immediate cash infusion helps businesses manage operational expenses and bridge cash flow gaps.

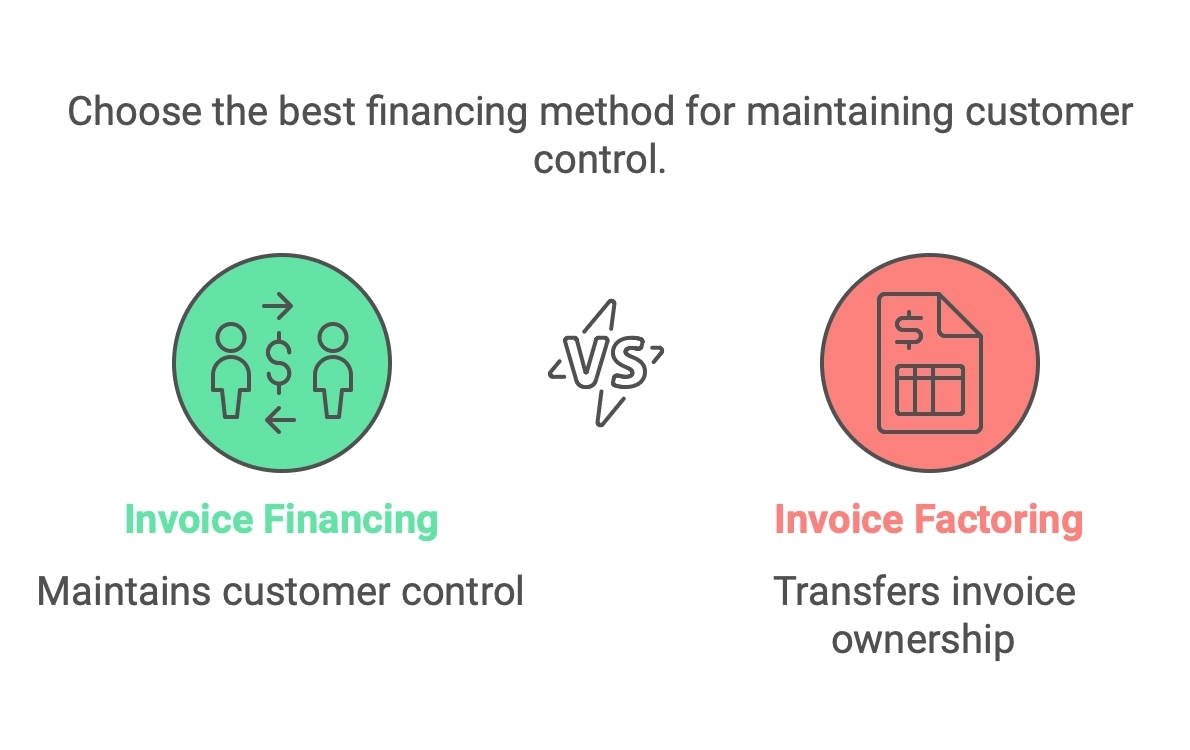

The remaining invoice balance, known as the reserve, is set aside until the customer’s payment arrives. Upon receiving payment, the financing company deducts a service fee, which covers costs and interest associated with the financing. The business then receives the remaining balance, concluding the transaction. This approach allows businesses to maintain control of their customer interactions, unlike invoice factoring, which involves transferring invoice ownership and collection responsibilities to a third party.

Certainly, let’s refine the section to ensure it aligns with the previously provided content and avoids repetition:

What are the main types of invoice financing?

Invoice financing offers businesses two principal methods, each with unique processes and benefits tailored to different operational needs: invoice factoring and invoice discounting. Grasping the nuances of these options can significantly aid in optimizing cash flow management while maintaining essential business relationships.

Invoice Factoring

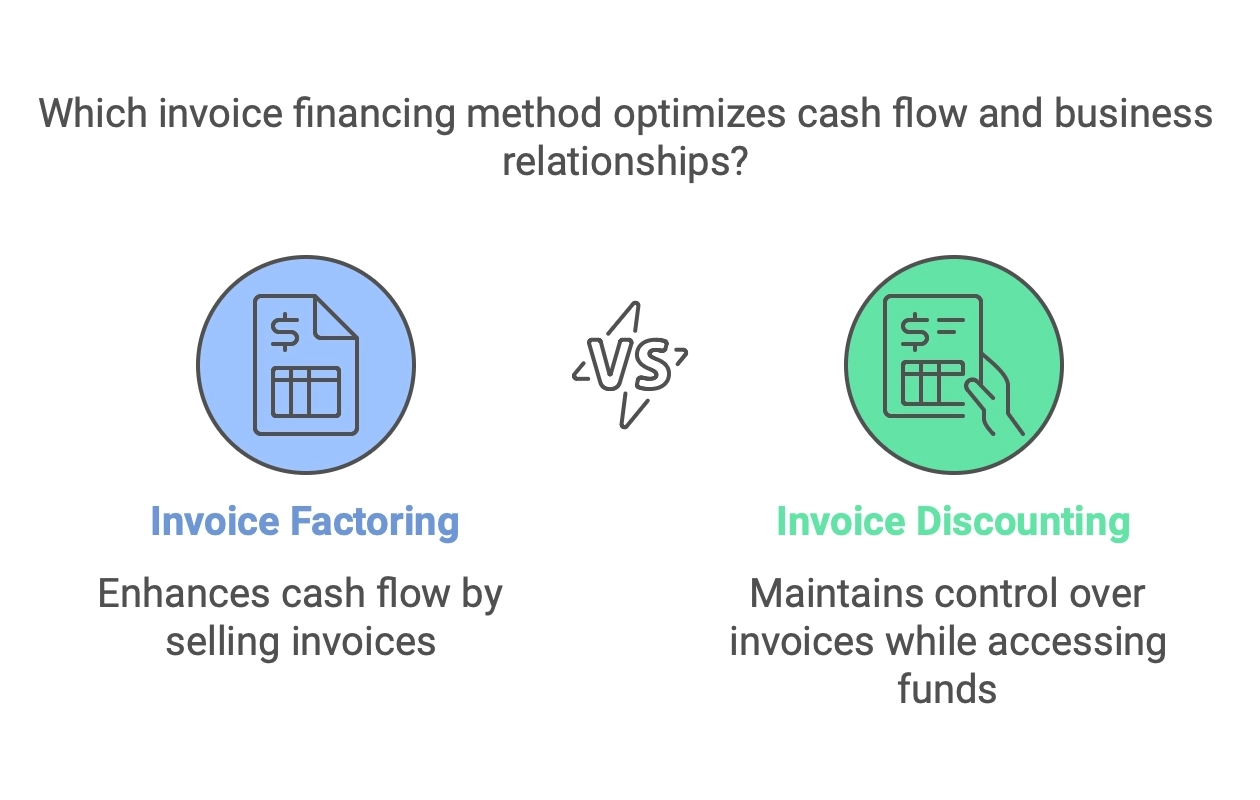

Invoice factoring involves transferring the ownership of outstanding invoices to a factoring company. This company assumes the role of collecting payments directly from customers, thereby relieving the business of the administrative load and associated risks. Businesses gain swift access to capital, which is advantageous for covering pressing financial obligations or facilitating growth initiatives.

Despite the immediate liquidity benefits, businesses must consider the impact on customer relationships, as the factoring company controls the collection process. This change can influence customer perceptions if the factoring entity’s practices differ from those of the business. Therefore, while factoring is effective for quick cash flow improvement, its effect on customer management needs careful evaluation.

Invoice Discounting

Unlike factoring, invoice discounting allows businesses to maintain control over their customer relationships and invoice collections. The financing company provides an advance based on the value of selected invoices, but the business continues to manage customer payments. This method preserves the confidentiality of the financing arrangement, keeping customer interactions unchanged.

While invoice discounting offers flexibility and discretion, it typically provides less extensive funding compared to factoring. Businesses must strategically assess which invoices to finance to maximize the benefits of this approach. Despite potential funding limitations, discounting enables businesses to manage cash flow subtly while retaining control over their client engagements.

Automate document processing with TurboDoc

Recognize invoices, contracts, and forms in seconds. No manual work or errors.

Try for free!

What are the benefits of invoice financing for businesses?

Engaging invoice financing can offer businesses a strategic advantage by swiftly converting accounts receivable into operational capital. This process provides businesses with an immediate cash flow boost, enabling them to cover essential expenses and invest in new projects without the delay of waiting for customer payments. This capability is particularly advantageous for those navigating extended payment cycles.

Unlike traditional debt solutions, invoice financing offers a quick and streamlined access to capital. Businesses benefit from a simplified approval process and less stringent requirements, making it an attractive option for startups and growing enterprises without extensive credit history or assets for collateral. By utilizing the value of their receivables, companies can secure the funds necessary to support ongoing operations and strategic growth initiatives.

The flexibility inherent in invoice financing allows businesses to choose specific invoices for financing, aligning with their unique financial strategies and customer dynamics. This selective approach ensures that only the most beneficial invoices are financed, maximizing liquidity while managing costs effectively. Moreover, partnering with an experienced financing company enables businesses to assess and manage customer credit risk more effectively. These companies offer valuable insights into credit evaluations, helping businesses make informed decisions on credit extensions and safeguarding their financial stability.

What are the potential drawbacks to consider?

While invoice financing presents numerous advantages, it is vital for businesses to consider potential drawbacks to determine if it aligns with their financial strategy. A primary concern is the associated cost. Invoice financing can be more expensive than traditional bank loans due to various fees and interest rates, which can affect overall profit margins. These costs can accumulate, making invoice financing less suitable for businesses prioritizing long-term, economical financing.

Another critical consideration is the reliance on prompt customer payments. The success of invoice financing depends heavily on customers paying their invoices on time. Delays or non-payments can disrupt expected cash flows and extend the financing period, resulting in additional costs. It is essential for businesses to assess the creditworthiness and payment reliability of their customers to mitigate potential financial disruptions.

For those opting for factoring, the potential loss of direct control over customer interactions is a significant factor. When a factoring company takes over invoice collection, businesses may lose personal contact with their clients regarding payment issues. This shift can impact customer satisfaction, especially if the third-party’s collection practices differ from the business’s usual approach. Moreover, businesses must adapt to the processes and systems of the financing company, which might not fully integrate with their existing operations, possibly causing inefficiencies that require careful management.

Lastly, invoice financing might not be the ideal solution for all business models, particularly those with smaller volumes or lower-value invoices. The benefits of invoice financing are often proportional to the volume and value of invoices; therefore, companies with fewer invoices may find the costs and processes do not justify the benefits. It is crucial for these businesses to conduct a detailed evaluation of their invoicing practices and explore whether other financing options might better fulfill their requirements.

To determine if invoice financing is the right fit, businesses should begin by analyzing their specific cash flow requirements. This involves identifying periods of financial strain due to delayed customer payments and assessing whether immediate access to funds through invoice financing could alleviate these pressures. By examining cash flow patterns, businesses can pinpoint when financing would provide the most strategic advantage.

A critical part of the decision-making process involves weighing the costs and terms of invoice financing against other financial solutions. This means a detailed comparison of fee structures, interest rates, and repayment conditions. Such an analysis helps businesses understand the financial implications of invoice financing relative to traditional loans or lines of credit, ensuring that the choice aligns with their broader financial goals.

Understanding the composition of the customer base and the value of invoices is also vital. Businesses with a stable, creditworthy clientele will likely benefit more from invoice financing, as this setup promises reliable cash flow. Evaluating the typical invoice size and customer payment history can reveal potential risks and benefits, allowing for a more informed financing decision.

Choosing between factoring and discounting requires careful consideration of business objectives and customer dynamics. Businesses must weigh the benefits of maintaining control over invoice collections against the convenience of outsourcing this task. This choice impacts not only cash flow management but also the quality of customer relationships, which are essential for long-term success.

Selecting financing partners with proven expertise in the relevant industry can provide additional confidence. These companies offer specialized insights and solutions tailored to sector-specific challenges, ensuring that businesses receive strategic support and guidance throughout the financing process.

Finally, adopting advanced invoice management solutions can further streamline the financing process. These tools enhance visibility and control over accounts receivable, simplifying tracking and management tasks. By integrating such technology, businesses can ensure that invoice financing becomes a seamless and highly effective component of their financial strategy.

By carefully evaluating your business’s unique cash flow needs, customer dynamics, and financial goals, you can determine if invoice financing is the right solution for your company. With the right approach and partners, this powerful tool can provide the liquidity and flexibility needed to navigate challenges and seize opportunities in today’s fast-paced business landscape. If you’re looking to streamline your invoice management and unlock the value of your receivables, start a free trial to experience TurboDoc’s invoice processing capabilities – we’re here to help you optimize your cash flow and achieve your growth objectives.

❓ Invoice Financing — FAQs

What is invoice financing and how does it work?

Invoice financing lets a business unlock cash tied up in unpaid invoices. You sell or borrow against invoices to a lender, get an advance immediately, and receive the remainder (minus fees) when the customer pays. Models include factoring (lender manages collections) and invoice discounting (you manage collections).

Who usually uses invoice financing?

Small and medium businesses, startups, and seasonal companies with long payment terms or fast growth often use invoice financing to smooth cash flow, pay suppliers, or fund expansion without waiting for customers to pay.

How do I qualify for invoice financing?

Lenders mainly evaluate your customers’ creditworthiness, the quality/age of invoices, and your business documentation. Requirements include issued invoices, proof of delivery or service, customer contact details, and business identity docs. Strong, dispute-free receivables improve approval chances.

How much does invoice financing cost?

Costs vary by provider. Fees may include a service/discount fee (percentage of invoice) and sometimes interest. The cost depends on invoice size, customer credit risk, and facility type (recourse vs non-recourse). Always request a full fee schedule and scenarios before committing.

What are the risks and disadvantages of invoice financing?

Risks include higher costs, possible customer concerns with third-party factors, liability in recourse facilities, dependency on financing, and complications if invoices are disputed or fraudulent.

Is invoice financing a good idea for my business?

It can help bridge short-term cash needs, scale quickly, or manage seasonality. Its value depends on fees vs alternatives, your customers’ reliability, and whether quick cash outweighs reduced margins. A pilot run helps measure impact.

How can I get out of invoice financing?

To exit, pay off outstanding advances and fees, settle disputes, and close the facility per contract terms. Plan an exit strategy such as securing a line of credit, improving collections, or negotiating terms with customers to avoid re-entering expensive financing.

What are alternatives to invoice financing?

Alternatives include business lines of credit, short-term loans, merchant cash advances, trade credit, early-payment discounts from customers, or better internal collections. Compare total costs, flexibility, and operational impact before deciding.